Ahead of your business exit, it is easy to focus on the headline valuation of your business. But it is often more important to think about how much income you’d like to receive each year (after tax) and whether the proceeds can fund the lifestyle you’d like in retirement.

With people living longer and wishing to retire earlier, the tax implications of post-sale proceeds need to be considered to ensure you don’t overpay throughout retirement.

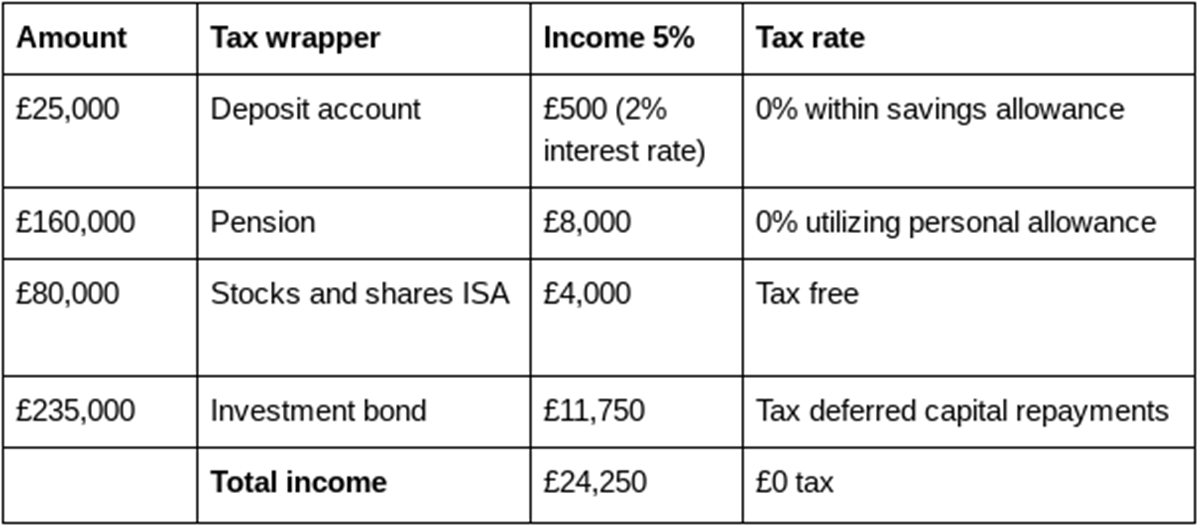

The importance of diversification across investments and assets is well known, but the benefit of diversifying across different tax structures is underappreciated. The combination of utilising your cash, pension, ISA, bonds and other tax-efficient ‘wrappers’ can lead to a very tax-efficient form of income.

Earnouts typically ranging between one and five years. As an example, the table below shows a potential structure, four years on from a £500,000 business sale after tax.

Maximising your pension allowances in the years ahead of retirement can be a great tax-efficient way of extracting cash from the business and can form the foundation of your retirement income strategy. Combining your pension with careful management and other tax-efficient investment vehicles will help you to squeeze the most value out of the sale.

- For further Lancashire business news, advice and analysis subscribe to Lancashire Business View or join the LBV Hub from just £2.50 per month. Click here to subscribe now.

Enjoyed this? Read more from James Freshney, Mattioli Woods